Guides

SEC Marketing Rule: Complete Compliance Guide (June 2026)

SEC Marketing Rule compliance guide for investment advisers in 2026: performance advertising, testimonials, endorsements, Form ADV, books and records, and audit-ready review workflows.

Glenn Espinosa··Updated ·10 min read

Article details

- Written by

- Glenn EspinosaCEO & Founder

- Topic

- Guides

- Published

- Dec 27, 2025

- Last updated

- Jun 19, 2026

- Reviewed by

- Luthor Team

Reviewed Jun 19, 2026 for source quality, practical relevance, and regulated-marketing context.

Updated June 19, 2026. This guide has been refreshed with current exam-readiness guidance, cleaner SEO metadata, updated internal links, and practical AI-assisted review controls for investment adviser marketing teams.

SEC-registered investment advisers that directly or indirectly disseminate an "advertisement" operate under the SEC Marketing Rule, Rule 206(4)-1 under the Investment Advisers Act of 1940. If you share performance results, publish client feedback, use testimonials, promote third-party ratings, or make statements about your advisory services, you are expected to back those claims with records that stand up during an SEC exam.

The 2026 compliance point is not just "know the rule." It is "prove the workflow." Advisers need policies, reviewer notes, substantiation files, final approved versions, disclosure evidence, and Form ADV alignment.

TLDR:

- The SEC Marketing Rule replaced more than 60 years of fragmented advertising guidance with seven general prohibitions governing adviser advertisements across channels.

- Performance ads require net-of-fee presentation, support for material assumptions, and full portfolio context for extracted performance.

- Testimonials, endorsements, and third-party ratings are permitted only when required disclosures, oversight, compensation terms, and recordkeeping are handled correctly.

- The SEC's April 2024 Marketing Rule risk alert and FY2025 Examination Priorities both make clear that examiners review the full compliance program, not just final copy.

- AI-assisted review can help, but advisers still need human accountability, source evidence, approval records, and complete books-and-records support.

What Is the SEC Marketing Rule?

The SEC Marketing Rule, formally known as Rule 206(4)-1 under the Investment Advisers Act of 1940, represents the most important update to investment adviser advertising regulations in over six decades. It governs advertisements by registered investment advisers, including many digital and indirect communications that older advertising guidance did not address cleanly.

In practice, the rule affects:

- Website copy and landing pages

- Advisor bios and social posts

- Email campaigns and newsletters

- Videos, podcasts, webinars, and scripts

- Pitch decks and PDFs

- Performance presentations

- Testimonials, endorsements, reviews, and third-party ratings

- Paid referral, influencer, or solicitor-style arrangements

If the content offers advisory services to prospects or promotes new advisory services to current clients, treat it as a potential advertisement and document the review.

What Is New for 2026 Exam Readiness?

The Marketing Rule itself is not new in 2026, but examiner expectations are clearer. The SEC Division of Examinations' April 2024 Risk Alert described preliminary observations from Marketing Rule exams, including issues involving policies and procedures, substantiation, books and records, and Form ADV disclosures.

The SEC's FY2025 Examination Priorities also state that examinations of adviser compliance programs typically include core areas such as marketing, valuation, trading, portfolio management, disclosure and filings, and custody. That matters because Marketing Rule compliance is tested as part of the broader Rule 206(4)-7 compliance program.

For 2026, the practical standard is:

- Can you identify every public-facing advertisement?

- Can you show who reviewed it and when?

- Can you substantiate every material claim?

- Can you prove required disclosures were included near the claim?

- Can you connect the final asset to books-and-records evidence and Form ADV disclosures?

The Seven General Prohibitions under the Marketing Rule

The Marketing Rule sets seven baseline prohibitions that apply to all advertisements. Violating any one of these prohibitions may result in non-compliance.

- Untrue Statements of Material Fact: Advertisements may not include false statements, or technically accurate statements that create a misleading overall impression, about material facts that could influence an investor’s decision.

- Material Omissions: Leaving out information necessary to make a statement not misleading violates the rule, even if the statement itself is factually correct.

- Unsubstantiated Claims: Advisers may not make claims implying specific results or outcomes without a documented reasonable basis supporting the representation.

- Unbalanced Benefit Discussions: Discussions of potential benefits must be balanced with material risks or limitations; presenting upside without fair risk disclosure is prohibited.

- Cherry-Picked Performance: References to specific profitable recommendations require prescribed context about all recommendations in the same category over a defined period.

- Improper Testimonials or Endorsements: These are restricted unless you meet specific disclosure and other conditions outlined in the rule.

- Improper Use of Third-Party Ratings: You cannot use ratings without required disclosures about methodology and compensation arrangements.

Defining Advertisement under the Marketing Rule

The Marketing Rule captures far more content than the 1961 rule through two distinct prongs.

- Direct and Indirect Communications: Any direct or indirect communication that offers an adviser’s investment advisory services to prospective clients or investors, or promotes new advisory services to existing clients (subject to limited exclusions, including a general one-on-one communications carve-out).

- Compensated Endorsements and Testimonials: Any endorsement or testimonial for which an adviser provides cash or non-cash compensation, directly or indirectly.

Performance Advertising Requirements and Restrictions

Performance advertising often receives heightened regulatory attention because returns influence investor decisions more than any other factor.

- Net Performance Presentation: Present performance net of fees, or give investors the data to calculate net returns when showing gross figures. Gross-only presentations misrepresent what clients actually earn. When an advertisement presents “net performance,” it must reflect the deduction of advisory fees and any other fees and expenses a client or investor paid or would have paid in connection with the adviser’s services (as applicable to the performance being shown).

- Extracted Performance: You may use it only if you provide or offer the full portfolio performance from which you extracted the subset, covering the same time period.

- Hypothetical Performance: Hypothetical performance shows results that never occurred. Required steps include adopting written policies covering criteria for use, documenting a reasonable basis for the projections, and disclosing information that helps investors understand limitations and key assumptions.

Testimonials, Endorsements, and Third-Party Ratings

The Marketing Rule permits testimonials, endorsements, and third-party ratings for the first time since 1961. Permission requires mandatory disclosure and oversight.

Required Disclosures

Disclose whether the promoter is a current client. When you compensate the promoter (cash or non-cash), disclose that fact and describe material conflicts created by the compensation arrangement. For third-party ratings, disclose the period covered, methodology criteria, and any compensation paid.

Disclosures must appear in proximity to the testimonial or rating itself.

Oversight and Documentation

Written agreements with compensated promoters are generally required, unless the promoter is an affiliate of the adviser or the promoter receives de minimis compensation (generally $1,000 or less, or equivalent non-cash value, during the preceding 12 months). You must have a reasonable basis to believe the promoter complies with the rule's requirements.

Books and Records Requirements for Marketing Materials

Rule 204-2 requires advisers to keep specific records for all marketing materials. The SEC uses these records during exams to verify compliance claims.

- Materials Subject to Retention : Document all material factual statements in each advertisement. Claims about assets under management, client numbers, team credentials, or investment approaches require supporting evidence.

- Performance and Third-Party Rating Records: Retain data and calculations used for performance presentations (such as account records, composite construction materials, fee schedules, and methodology documentation). For third-party ratings, keep questionnaires and supporting information provided to the rating organization.

- Retention Period and Accessibility: Keep records for five years from the advertisement’s last use, with the first two years maintained in an easily accessible location so records can be produced promptly during exams.

An exam-ready record should include the original draft, final approved version, reviewer comments, approval timestamp, source files for factual claims, performance calculations, disclosure text, channel and audience metadata, and any post-publication changes. If AI participated in the review, keep the AI finding, model or ruleset version, reviewer decision, and override rationale as part of the record.

SEC Enforcement Actions and Sweep Examination Findings

The SEC’s Marketing Rule enforcement sweep began with settled charges against nine investment advisers announced on September 11, 2023. Those cases focused on hypothetical performance advertised to the general public without the required policies and procedures. The SEC also noted that two advisers failed to maintain required copies of their advertisements.

Violations identified during sweeps include:

- Hypothetical Performance Without Required Policies: Firms advertised hypothetical performance to general audiences without policies and procedures designed to ensure relevance to the likely financial situation and investment objectives of the intended audience.

- Misrepresenting Third-Party Ratings: Advisers cited ratings from organizations that never assessed them or mischaracterized ranking methodologies to prospects.

- Failing to Disclose Testimonial Arrangements: Firms published client endorsements without disclosing compensation or failed to clarify whether endorsers were current clients. Others shared ratings without explaining the evaluation period or criteria.

- Missing Advertisement Records: Firms could not produce required copies or supporting evidence for materials they had used publicly.

Common Compliance Deficiencies Found During SEC Examinations

The SEC Division of Examinations issued an April 2024 Risk Alert sharing preliminary observations from recent examinations of advisers’ compliance with the Marketing Rule, the Compliance Rule, the Books and Records Rule, and related Form ADV disclosures.

Cherry-Picked Performance Data

Firms presented selective performance data without required context:

- Showing only top-performing accounts while excluding similar accounts with lower returns

- Showing gross returns without providing information investors need to calculate net results

Social Media Violations

Posts focused on investment benefits without addressing associated risks. Brief formats do not excuse firms from balanced presentation requirements. LinkedIn posts, advisor videos, comments on testimonial content, and boosted posts should all be treated as reviewable marketing surfaces when they promote advisory services.

Documentation Requirements

Examiners routinely request complete copies of all advertisements spread during the examination period, Form ADV Part 2A disclosures explaining marketing practices, and source documents substantiating every factual claim. Firms unable to produce contemporaneous records face findings. Maintain organized, immediately accessible proof for every statement you publish.

Form ADV Disclosure Updates for Marketing Practices

Form ADV Item 5.L requires advisers to disclose whether they use performance advertising. Check yes if you present gross or net returns, time-weighted or dollar-weighted performance, extracted performance, hypothetical performance, or related performance to current or prospective clients.

Part 2A disclosures require plain-language descriptions of your marketing practices. Describe when and how you use performance presentations. Explain testimonial or endorsement arrangements, including who provides them and whether you pay cash or non-cash compensation. If you reference third-party ratings, identify the organizations that provide them and disclose any payments made for ratings or promotional use.

Update Form ADV responses so they are accurate, but note that Form ADV does not require advisers to promptly update Item 5 (including Item 5.L “Marketing Activities”) via an other-than-annual amendment; advisers typically update these responses in the annual updating amendment, even though exam staff may inspect whether the answers reflect current practices.

Policies and Procedures Requirements for Marketing Rule Compliance

Rule 206(4)-7 requires written policies and procedures reasonably designed to prevent Marketing Rule violations. The SEC assesses whether your policies exist and whether you follow them. Documentation provides no defense when advertisements violate the rules your policies prohibit.

Develop performance calculation methodologies that comply with net presentation, extracted performance conditions, and hypothetical performance criteria.

Include oversight procedures for testimonials, endorsements, and third-party ratings. Detail how you screen promoters, execute written agreements, verify disclosures appear, and monitor ongoing compliance. Policies should cover recordkeeping responsibilities and retention schedules.

How AI-Assisted Review Fits the SEC Marketing Rule

AI can help advisers identify risky marketing language before content reaches a human reviewer. The most useful checks include:

- Detecting testimonials, endorsements, and third-party ratings

- Flagging gross-only or extracted performance claims

- Identifying missing or weak disclosure proximity

- Extracting factual claims that need substantiation

- Comparing claims against approved source documents

- Checking Form ADV consistency

- Logging reviewer decisions and final versions

AI should not be treated as the final legal reviewer for complex or high-risk advertising. For Marketing Rule purposes, the defensible pattern is AI first-pass review plus human approval, with the system preserving both the AI finding and the human decision. See our broader AI marketing compliance guide for agent governance, logging, and human-in-the-loop controls.

Building an Audit-Ready Marketing Compliance Program with Luthor

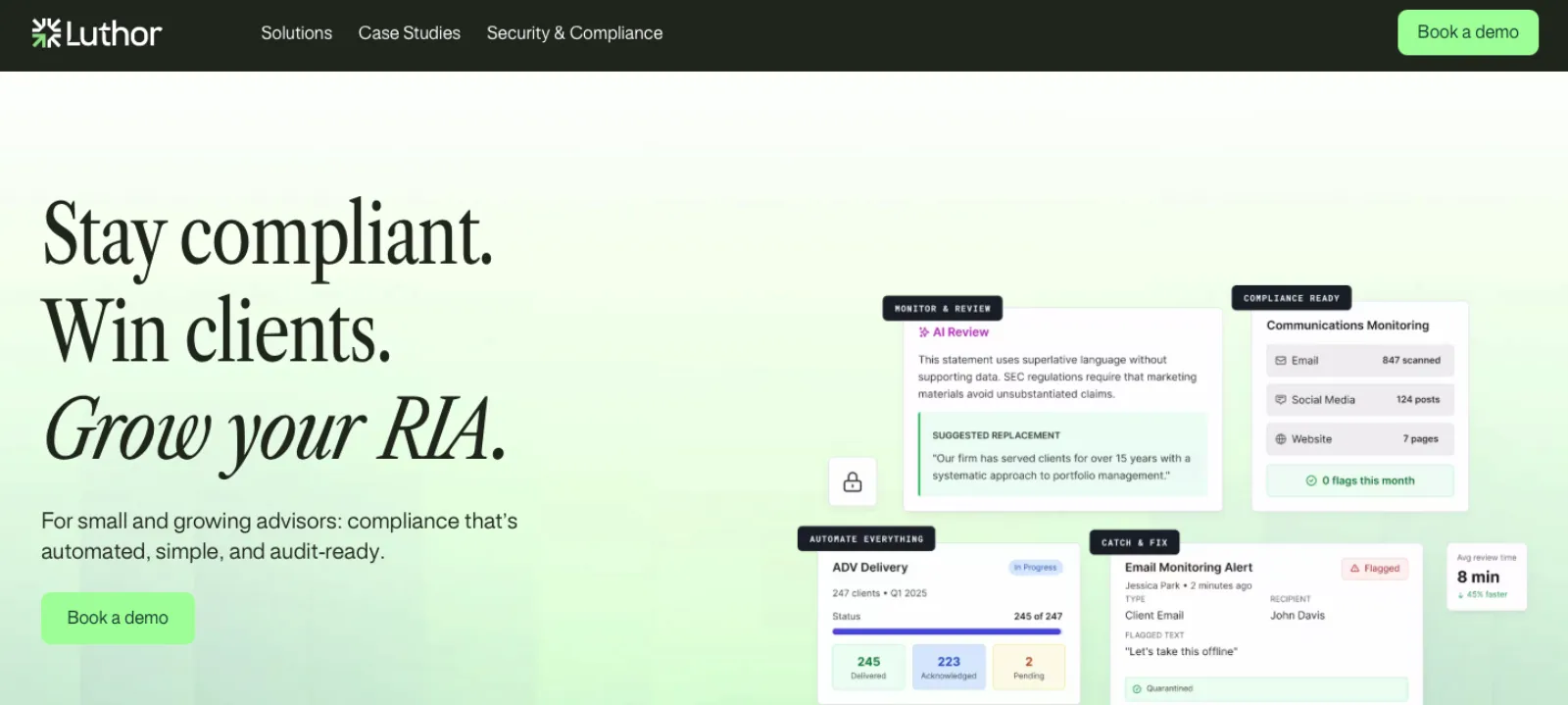

Maintaining Marketing Rule compliance isn’t about periodic cleanups anymore, it requires continuous oversight, documentation, and version control across every channel an adviser uses. Luthor is built for exactly that reality.

Luthor’s AI-powered marketing review engine scans web pages, emails, PDFs, decks, and social posts for issues tied to performance claims, testimonials, endorsements, unbalanced language, and missing disclosures. It monitors live sites and advisor pages so approved materials don’t drift out of compliance over time. When something changes, Luthor flags the update, explains the rule at issue, and suggests compliant alternatives.

Every version, approval, disclosure, and rationale is captured automatically in a tamper-evident archive that satisfies SEC Rule 204-2 expectations, making exam response far more efficient. Firms avoid the scramble of reconstructing records because documentation is created as content is produced.

For small and mid-sized advisers, Luthor functions like an outsourced CCO augmented with AI, keeping marketing teams fast, compliance teams informed, and public content aligned with the SEC Marketing Rule year-round.

FAQs

What is the difference between a testimonial and an endorsement under the SEC Marketing Rule?

A testimonial is a statement by a current client about their experience or advice received from your firm. An endorsement is any statement by any person, client or non-client, that refers or promotes your services. All testimonials are endorsements, but endorsements can come from non-clients like industry experts or influencers.

How do I calculate net performance correctly for marketing materials?

Deduct your advisory fees plus all other account-level fees and expenses that reduce client returns. Gross-only presentations violate the rule because they misrepresent what clients actually earn. You must either show net performance directly or provide investors with the data needed to calculate net returns themselves.

When can I show extracted performance from a single investment?

You may present results from select investments only when you provide or offer the complete portfolio performance from which you extracted the subset, covering the same time period. Both data sets must receive equal or greater prominence so investors can view the subset alongside total portfolio results.

Are social media posts advertisements under the SEC Marketing Rule?

They can be. A social media post is more likely to be an advertisement if it offers advisory services, promotes new advisory services, discusses performance, includes testimonials or endorsements, or is part of a paid or compensated promotional arrangement. Firms should preserve both static posts and relevant review records.

What Marketing Rule records should an RIA keep?

Keep the final advertisement, prior material versions, reviewer notes, approval timestamps, substantiation for material factual statements, performance calculations, testimonial or endorsement disclosures, promoter agreements where required, Form ADV support, and evidence of where and when the asset was used.

Can AI review SEC Marketing Rule content?

Yes, AI can support first-pass review by flagging risky claims, missing disclosures, testimonial language, performance issues, and substantiation gaps. Human review remains important for final approval, exceptions, legal interpretation, and high-risk performance or endorsement content.

Does Form ADV need to match marketing practices?

Yes. Item 5.L and Part 2A should accurately reflect the adviser's marketing practices, including performance advertising, testimonials, endorsements, and third-party ratings. Examiners may compare public marketing against Form ADV disclosures during an exam.

Final thoughts on Marketing Rule compliance strategies

Staying compliant with the SEC Marketing Rule goes beyond knowing the text of the regulation; it requires consistent documentation, clear review routines, and records that hold up during an exam. Sweep findings show that regulators check every statement against its source, which means firms need substantiation files created at the time content is produced, not after the fact. Regular internal checks help keep marketing practices aligned with actual disclosures, and tools like Luthor can support these efforts by reviewing content, capturing evidence, and helping firms keep public materials in a steady exam-ready state.

Keep reading

Related resources

Guides

How to Use AI for Marketing Compliance in 2026

A practical 2026 guide to AI marketing compliance: agent supervision, review workflows, privacy controls, audit trails, and human approval for regulated teams.

16 min

Guides

RIA Compliance Software: Best Solutions For Investment Advisors

RIA compliance software solutions for registered investment advisors. Can they really streamline SEC compliance tasks?

10 min

Guides

Advertising Compliance Checklist for RIAs & FinTech

Our complete advertising compliance checklist helps you avoid fines. Covers SEC rules, FTC guidelines, disclosures, and more.

15 min

Never publish risk again.

Our policy and legal engineers will walk through your content workflows and regulatory obligations, then integrate Luthor in days, not months.